PNNL-23923 Rev1

Methodology for Evaluating Cost-

effectiveness of Commercial Energy

Code Changes

R Hart

B Liu

August 2015

Prepared for

the U.S. Department of Energy

under Contract DE-AC05-76RL01830

Prepared by

Pacific Northwest National Laboratory

Richland, Washington 99352

iii

Summary

This document lays out the U.S. Department of Energy’s (DOE’s) methodology for evaluating the

cost-effectiveness of energy code and standard

1

proposals and editions. The evaluation is applied to new

provisions or editions of ANSI/ASHRAE/IES

2

Standard 90.1 and the International Energy Conservation

Code. The methodology follows standard life-cycle cost (LCC) economic analysis procedures. Cost-

effectiveness evaluation requires three steps: 1) evaluating the energy and energy cost savings of code

changes, 2) evaluating the incremental and replacement costs related to the changes, and 3) determining

the cost-effectiveness of energy code changes based on those costs and savings over time.

Cost-effectiveness can be evaluated for an individual code change proposal or an entire edition-to-

edition upgrade of an energy code. Multiple parties are interested in building energy codes, and they have

different economic viewpoints. To account for this, and the fact that the ASHRAE Standing Standard

Project Committee (SSPC) 90.1 has established an economic analysis procedure, three scenarios have

been established for the cost-effectiveness methodology:

1. Scenario 1 (also referred to as the Publicly-Owned Method): LCC analysis method representing

government or public ownership (without borrowing or taxes).

2. Scenario 2 (also referred to as the Privately-Owned Method): LCC analysis method representing

private or business ownership (includes loan and tax impacts).

3. Scenario 3 (also referred to as the ASHRAE 90.1 Scalar Method): Represents a pre-tax private

investment point of view, and uses economic inputs established by the ASHRAE SSPC 90.1.

In evaluating code change proposals and assessing new editions of commercial building energy

codes, DOE intends to calculate multiple metrics selected from the following:

• Life-cycle cost net savings (a.k.a., net present value (NPV) of savings)

• Savings-to-investment ratio (SIR)

• The ASHRAE 90.1 scalar ratio

• Simple payback period

NPV of savings based on LCC is the primary metric DOE intends to use to evaluate whether a

particular code change is cost-effective. Any code change that results in an NPV of savings greater than

to zero (i.e., monetary benefits exceed costs) will be considered cost-effective. The payback period,

scalar ratio, and SIR analyses provide additional information DOE believes is helpful to other participants

in code change processes and to states and jurisdictions considering adoption of a new code.

Economic parameters are chosen to represent the economic impact of a typical commercial building

ownership or tenant situation. DOE’s approach is to consult appropriate sources of publicly available

information to establish assumptions for each financial, economic, and energy price parameter, following

1

Throughout this document, when referring to energy codes, energy standards are included, as they become adopted

into code, and are evaluated for their impact as an adopted code.

2

ANSI – American National Standards Institute; ASHRAE – American Society of Heating, Refrigerating and Air-

Conditioning Engineers; IES – Illuminating Engineering Society; IESNA – Illuminating Engineering Society of

North America (IESNA rather than IES was identified with Standard 90.1 prior to 90.1-2010)

iv

the guidelines established in this methodology. DOE intends to update parameters for future analyses to

account for changing economic conditions, and document the source of each parameter in the specific

analysis.

v

Acknowledgments

This report was prepared by Pacific Northwest National Laboratory (PNNL) for the U.S. Department

of Energy (DOE) Building Energy Codes Program. The authors would like to thank David Cohan,

Jeremy Williams, and Mohammed Khan at DOE for providing oversight. This work was truly a team

effort, and the authors would like to express their deep appreciation to everyone from the PNNL codes

team who contributed to its completion, including especially Michael Rosenberg, Matt Wilburn, Todd

Taylor, Vrushali Mendon, and Mark Halverson.

Reid Hart, PE

Pacific Northwest National Laboratory

vii

Acronyms and Abbreviations

ANSI American National Standards Institute

ASHRAE American Society of Heating, Refrigerating and Air-Conditioning Engineers

BECP Building Energy Codes Program

DEER Database for Energy Efficient Resources

DOE U.S. Department of Energy

EIA Energy Information Administration

EISA Energy Independence and Security Act of 2007

FEMP Federal Energy Management Program

HVAC heating, ventilating, and air-conditioning

ICC International Code Council

IECC International Energy Conservation Code

IES Illuminating Engineering Society

LCC life-cycle cost

MEP mechanical, electrical, and plumbing

MHC McGraw-Hill Construction

NIST National Institute of Standards and Technology

NPV net present value

PNNL Pacific Northwest National Laboratory

PPI Producer Price Index

SIR savings-to-investment ratio

SSPC Standing Standard Project Committee

ix

Contents

Summary ...................................................................................................................................................... iii

Acknowledgments ......................................................................................................................................... v

Acronyms and Abbreviations ..................................................................................................................... vii

1.0 Introduction ....................................................................................................................................... 1.1

1.1 Need for Cost-effectiveness Analysis ....................................................................................... 1.1

1.2 Evaluating Cost-effectiveness ................................................................................................... 1.3

2.0 Estimating the Energy and Energy Cost Savings of Code Changes ................................................. 2.1

2.1 Building Energy Use Simulation ............................................................................................... 2.1

2.1.1 Energy Simulation Tool ................................................................................................. 2.1

2.1.2 Building Prototypes ........................................................................................................ 2.2

2.1.3 Default Inputs ................................................................................................................. 2.3

2.1.4 Provisions Requiring Special Consideration .................................................................. 2.4

2.2 Weather Locations..................................................................................................................... 2.4

2.3 Energy Cost Savings ................................................................................................................. 2.5

3.0 Estimating the Incremental Costs of Code Changes .......................................................................... 3.1

3.1 Cost Estimating Approach ........................................................................................................ 3.1

3.2 Sources of Cost Estimates ......................................................................................................... 3.2

3.2.1 Approach to Cost Data Collection .................................................................................. 3.2

3.2.2 Economies of Scale and Market Transformation Effects ............................................... 3.3

3.2.3 Addressing Code Changes with Multiple Approaches to Compliance .......................... 3.4

3.3 Cost Parameters ......................................................................................................................... 3.5

3.4 Cost Updating for Inflation ....................................................................................................... 3.6

3.5 Cost Estimate Spreadsheet Workbook ...................................................................................... 3.6

4.0 Estimating the Cost-effectiveness of Code Changes ......................................................................... 4.1

4.1 Cost-effectiveness Analysis ...................................................................................................... 4.1

4.1.1 Economic Scenarios ....................................................................................................... 4.1

4.1.2 Cost-effectiveness Methodology .................................................................................... 4.2

4.2 Economic Metrics ..................................................................................................................... 4.4

4.2.1 Life-Cycle Cost Net Savings .......................................................................................... 4.5

4.2.2 Savings-to-Investment Ratio .......................................................................................... 4.6

4.2.3 Scalar Ratio .................................................................................................................... 4.6

4.2.4 Simple Payback Period ................................................................................................... 4.6

4.2.5 Economic Metric Summary............................................................................................ 4.7

4.3 Economic Parameters and Other Inputs .................................................................................... 4.8

4.3.1 Scenario 1: Publicly-Owned Method Parameters........................................................... 4.9

4.3.2 Scenario 2: Privately-Owned Method Parameters ......................................................... 4.9

x

4.3.3 Scenario 3: ASHRAE 90.1 Scalar Method Parameters ................................................ 4.12

4.3.4 Detailed Discussion of Economic Parameters .............................................................. 4.13

5.0 Aggregating Energy and Economic Results ...................................................................................... 5.1

5.1 Weighting Factors: Building Types and Climate Zones ........................................................... 5.1

5.2 Building Prototype Selection .................................................................................................... 5.3

5.3 Represented HVAC Equipment Types...................................................................................... 5.3

5.4 Aggregation across Building Type and Climate Zone .............................................................. 5.4

5.4.1 National and State-Level Aggregations ......................................................................... 5.5

5.4.2 Demonstration of Aggregate Cost-effectiveness ............................................................ 5.5

5.5 Supplemental Range of Results or Sensitivity Analysis ........................................................... 5.5

6.0 References ......................................................................................................................................... 6.1

Current Cost-effectiveness Parameters................................................................................. A.1 Appendix A

Supplemental Range of Results Method................................................................................B.1 Appendix B

xi

Tables

Table 2.1. Commercial Prototype Building Basic Characteristics ............................................................ 2.3

Table 2.2. Climate Locations Used in Energy Simulations ...................................................................... 2.5

Table 3.1. Example Sources of Cost Estimates by Cost Category ............................................................ 3.2

Table 3.2. Cost Estimate Adjustment Parameters ..................................................................................... 3.5

Table 4.1. Economic Metrics .................................................................................................................... 4.7

Table 4.2. Economic Parameters Required for Cost-effectiveness Metrics .............................................. 4.8

Table 4.3. Economic Parameters and Their Symbols ............................................................................... 4.9

Table 4.4. Present Value Cost and Benefit Components for Scenario 2 ................................................. 4.11

Table 4.5. Scalar Method Economic Parameters and Scalar Ratio Limit ............................................... 4.12

Table 5.1. National Weighting factors by Prototype ................................................................................. 5.2

Table 5.2. Commercial Weighting Factors by Climate Zone ................................................................... 5.2

Table 5.3. Prototype Buildings ................................................................................................................. 5.3

Table 5.4. HVAC Primary and Secondary Equipment ............................................................................. 5.4

1.1

1.0 Introduction

The U.S. Department of Energy (DOE)

1

has developed and established a methodology for evaluating

the energy and economic performance of commercial energy codes. This methodology serves two

primary purposes. First, as DOE participates in the codes and standards development processes, DOE

will use the methodology described herein, where appropriate, to ensure that DOE’s proposals are both

energy efficient and cost-effective. Second, when a new edition of ANSI/ASHRAE/IES

2

Standard 90.1 is

published, DOE will evaluate the new standards and codes

3

as a whole to estimate expected energy

savings and assess cost-effectiveness, which will help inform states and local jurisdictions interested in

adopting the new codes. DOE may also evaluate the cost-effectiveness of new editions of the

International Energy Conservation Code (IECC). DOE’s measure of cost-effectiveness balances longer-

term energy savings against increases to initial costs through a life-cycle cost (LCC) perspective.

1.1 Need for Cost-effectiveness Analysis

Section 307 of the Energy Conservation and Production Act, as amended, directs DOE to support

voluntary building energy codes by providing “assistance in determining the cost-effectiveness and the

technical feasibility of the energy efficiency measures included in such standards and codes” (42 U.S.C.

6836(a)(3))

and by periodically reviewing the technical and economic basis of the voluntary building

energy codes and seeking adoption of all technologically feasible and economically justified energy

efficiency measures and otherwise participating in any industry process for review and modification of

such codes (42 U.S.C. 6836(b)(2) and (3)).

The methodology described here supports DOE in fulfilling its charge to evaluate energy codes and

energy code proposals. Where evaluation of the cost-effectiveness of codes is required, DOE intends to

follow the procedures and use the parameters presented here. In some cases, DOE may rely on extant

cost-effectiveness studies directly addressing the building elements involved in a proposed change, if such

can be identified. When evaluating code changes proposed by entities other than DOE,

4

DOE may rely

on energy savings estimates, cost estimates, or cost-effectiveness analyses provided by the proponent(s)

or others if DOE deems the estimates and calculations credible.

1

Throughout this document, DOE is identified as the primary actor in developing and applying the discussed cost-

effectiveness methodology. In this activity, DOE has and will use outside resources, including the work of other

parties, such as the National Laboratories, to achieve its goal of evaluating cost-effectiveness of code proposals.

DOE engages in this activity through the Buildings Technology Office, and uses resources from other divisions in

DOE, including the Federal Energy Management Program (FEMP) and the Energy Information Administration

(EIA).

2

ANSI – American National Standards Institute; ASHRAE – American Society of Heating, Refrigerating and Air-

Conditioning Engineers; IES – Illuminating Engineering Society; IESNA – Illuminating Engineering Society of

North America (IESNA rather than IES was identified with Standard 90.1 prior to 90.1-2010)

3

Throughout this document, when referring to energy codes, energy standards are included, as they become adopted

into code, and are evaluated for their impact as an adopted code.

4

All code change proposals for ASHRAE Standard 90.1 are publicly available and are published by ASHRAE as

addenda for public review so that public comments can be considered by the committee in a consensus process that

follows ANSI procedures. The consensus process determines whether the code changes are approved for addition to

the next published edition of Standard 90.1.

1.2

Incremental first cost or cost-effectiveness information is requested by code development bodies for

proposals to energy codes. For example, the International Code Council (ICC) Code Development

Procedures (ICC 2014) require the following:

3.3.5.6 Cost Impact: The proponent shall indicate one of the following regarding the cost

impact of the code change proposal: 1) the code change proposal will increase the cost of

construction; or 2) the code change proposal will not increase the cost of construction.

The proponent shall submit information which substantiates either assertion. This

information will be considered by the code development committee and will be included

in the bibliography of the published code change proposal. Any proposal submitted

which does not include the requisite cost information shall be considered incomplete and

shall not be processed.

The ASHRAE 90.1 Standing Standard Project Committee (SSPC) discusses cost-effectiveness

analysis related to the ANSI consensus process on pages 1 and 4 of its recent work plan:

5

The main goal and primary responsibility is to publish a consensus standard in mandatory

language: That sets practical, technically feasible, and cost effective minimum energy

efficiency requirements for commercial buildings, except for low-rise residential

buildings, on a consistent time schedule. [Emphasis added]

…Thus, neither ASHRAE nor ANSI has an overt requirement for economic analysis, nor

for any other analysis for that matter, except that the SSPC must reach “consensus”

before a new standard will be approved by ANSI.

That said, the Committee has often used economic analysis in its decision-making

process and it continues to believe that economics play an important role in establishing

the requirements for a minimum national building energy efficiency standard.

Sometimes the Committee may desire a rigorous and detailed level of economic analysis,

while at other times intuitive professional judgment as to the economic impact of a

proposed new measure—without rigorous analysis—may be sufficient.

Thus, ICC requires cost, but not cost-effectiveness information, although such analysis often helps to

advance a proposal that increases the cost of construction. ASHRAE SSPC 90.1 sees benefit in cost-

effectiveness analysis, although it is not always seen as necessary in the consensus process. In both cases,

cost-effectiveness, where used during the code development process, is applied to individual code change

proposals and not codes as a whole. Many states

6

require or encourage cost-effectiveness analysis of the

energy code in adoption proceedings to demonstrate that overall the code has financial benefit to the

group of building users as a whole.

5

Work plan presented and approved at ASHRAE SSPC 90.1 meeting in June 2014, Seattle, New York State Energy

Conservation Construction Code Act WA.

6

As an example, section 11-101 of the New York State Energy Conservation Construction Code Act requires “such

code mandate that economically reasonable energy conservation techniques be used” and cost-effectiveness analysis

of energy codes is used in their adoption process. Available at:

http://public.leginfo.state.ny.us/LAWSSEAF.cgi?QUERYTYPE=LAWS+&QUERYDATA=$$ENG11-

101$$@TXENG011-101+&LIST=LAW+&BROWSER=BROWSER+&TOKEN=01053978+&TARGET=VIEW.

1.3

1.2 Evaluating Cost-effectiveness

Evaluating cost-effectiveness requires three primary steps: 1) evaluating the energy and energy cost

savings of code changes, 2) evaluating the incremental and replacement costs related to the changes, and

3) determining the cost-effectiveness of energy code changes based on those costs and savings over time.

The DOE methodology estimates the energy impact by simulating the effects of the code change(s) on

typical new commercial buildings, assuming both old and new code provisions are implemented fully and

correctly. The methodology does not estimate rates of code adoption or compliance. Cost-effectiveness

is defined primarily in terms of LCC evaluation, although the DOE methodology includes several metrics

intended to assist states considering adoption of new codes.

DOE intends to use the methodology described in this document to address DOE’s legislative

direction related to building energy codes. DOE also intends to use this methodology to inform its

participation in the update processes of ASHRAE Standard 90.1 and the IECC, both in developing code-

change proposals and in assessing the proposals of others when necessary. DOE further intends to use

this methodology in comparing the cost-effectiveness of new code editions to prior editions or existing

state energy efficiency codes.

The focus of this document is commercial buildings, which DOE defines in a manner consistent with

both Standard 90.1 and the IECC—buildings except one- and two-family dwellings, townhouses, and

low-rise (three stories or less above grade) multifamily residential buildings.

This document is arranged into four primary parts covering the following:

1. Estimating the Energy and Energy Cost Savings of Code Changes—by simulating changes to

representative building types. DOE defines commercial prototype buildings, establishes typical

construction and operating assumptions, and identifies climate locations to be used in estimating

impacts in all climate zones and all states. The building prototypes cover a range of the most typical

commercial buildings and include a variety of building system types (e.g., heating and cooling

equipment) to facilitate appropriate accounting for the energy use of different commercial

occupancies.

2. Estimating the Incremental Cost of Code Changes—by comparing the first cost of baseline buildings

to the first cost of buildings with the code implemented. Incremental replacement and maintenance

costs are also accounted for. A combination of methods is used to arrive at a national incremental

cost, and then adjustment factors are applied to arrive at incremental costs appropriate for states.

3. Estimating the Cost-effectiveness of Code Changes—by comparing energy cost savings to increases

in the first cost of the buildings. The methodology defines four metrics—net present value (NPV) of

savings, savings-to-investment ratio (SIR), scalar ratio, and simple payback period—that may be

calculated. It also establishes sources for the economic parameters to be used in estimating those

metrics and identifies sources of energy-efficiency measure costs.

4. Aggregating Energy and Economic Results—across building types and climate locations. The

methodology establishes sources for weighting factors to be used in aggregating location- and

building-type-specific results to state, national, climate zone, or other domain results.

2.1

2.0 Estimating the Energy and Energy Cost

Savings of Code Changes

The first step in assessing the impact of a code change or a new code is estimating the energy and

energy cost savings of the associated changes. DOE will usually employ computer simulation analysis to

estimate the energy impact of a code change. (Situations in which other analytical approaches might be

preferred are discussed later.) Where credible energy savings estimates are not available, DOE intends to

conduct analysis using an appropriate building energy estimation tool. In most cases, DOE intends to use

the EnergyPlus™ (EnergyPlus 2011) software as the primary tool for its analyses. If necessary to more

accurately capture the relevant impacts of a particular code change, DOE may supplement EnergyPlus

with other software tools, research studies, or performance databases. Such code changes will be

addressed case by case.

Code changes affecting a particular climate zone will be simulated in a weather location

representative of that zone. Where a code change affects multiple climate zones, DOE intends to produce

an aggregate (national or state) energy impact estimate based on simulation results from weather locations

representative of each zone, weighted to account for estimated new commercial construction by zone and

the fraction of specific building types that will be affected by the code change. Code changes affecting a

particular climate zone will be simulated in representative weather locations. DOE’s methodology

includes weighting factors based on recent new building construction data to allow the individual location

results to be aggregated to climate-zone and national averages as needed. These methodologies,

weighting factors, and aggregation approaches are described in Section 5.0.

2.1 Building Energy Use Simulation

The energy performance of most energy-efficiency measures in the scope of building energy codes

can be estimated by computer simulation. In estimating the energy performance of pre- and post-revision

codes, two building cases will be analyzed: 1) a building that complies with the pre-revision code and

2) an otherwise identical building that complies with the revised code under analysis. These two building

cases will be simulated in a variety of locations to estimate the overall (national average) energy impact

of the new code or code proposal. The inputs used in those simulations are discussed in the following

sections.

2.1.1 Energy Simulation Tool

DOE intends to use a whole building simulation tool to calculate annual energy consumption for

relevant end uses. For most situations, the EnergyPlus software, developed by DOE, will be the tool of

choice. EnergyPlus provides for detailed time-step (hourly or shorter time steps are typical) simulation of

a building’s energy consumption throughout a full year, based on typical weather data for a given

location. It covers most aspects of building systems impacting energy use in commercial buildings:

envelopes; heating, ventilating, and air-conditioning (HVAC) equipment and systems; water heating

equipment and systems; lighting systems; and plug and process loads. Depending on how building

energy codes evolve, it may be necessary to identify additional tools to estimate the impacts of some

changes. For example, inputs to EnergyPlus are often established with survey data, separate engineering

calculations, or ancillary analysis programs, as some systems are not directly covered within EnergyPlus

2.2

(e.g., elevator operation, swimming pools, and two-dimensional heat transfer through assemblies of

building materials).

DOE recognizes there are other tools that can produce credible energy estimates. DOE intends to use

EnergyPlus as its primary tool because it includes advanced simulation capabilities, is under active

development, is recognized as one of the leading simulation tools, and has the potential to include

capabilities either unavailable or less sophisticated in other accepted simulation tools. EnergyPlus has

capabilities for detailed simulation of complex HVAC systems, advanced capabilities for simulating

interaction between primary and secondary HVAC systems, and the potential for analyzing detailed

control strategies.

2.1.2 Building Prototypes

Separate simulations are typically conducted for multiple commercial building prototypes. The

prototypes used in the simulations are intended to represent a cross section of common commercial

building types covering 80% of new commercial construction. DOE developed 16 prototype building

models, which were reviewed extensively by building industry experts on ASHRAE SSPC 90.1 during

development and assessment of multiple editions of ASHRAE Standard 90.1. These prototype models,

their detailed characteristics, and their development are published on DOE’s Building Energy Codes

Program (BECP) web site.

1

A detailed description of the prototypes can also be found in a technical

report published by Pacific Northwest National Laboratory (PNNL), Energy and Cost Savings Analysis of

ASHRAE Standard 90.1-2010 (Thornton et al. 2011). The prototype models are further described in detail

in the quantitative determination of the energy savings of Standard 20.1-2013 (Halverson et al. 2014).

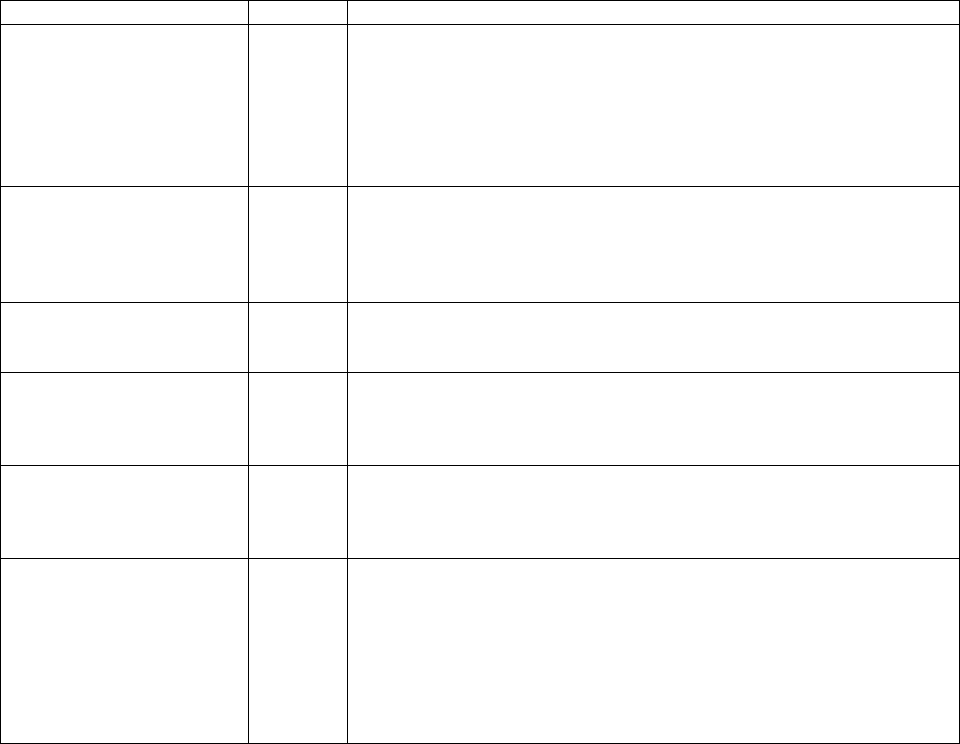

Table 2.1 shows the general characteristics DOE intends to use in analyzing the prototypes. Note that any

of the prototype characteristics may be modified if a code change impacts it or such modification adds

accuracy to the energy savings estimate for particular code changes.

DOE may select a subset of these prototype buildings and simulate them in representative climate

locations for the cost-effectiveness analysis to represent most of the energy and cost impacts of the code

changes in a particular code or proposal analysis. This approach is based on the fact that not all code

requirements will apply to a set of standardized prototypes. The overall savings of a code edition will be

well characterized if the preponderance of code measures and climate zones are directly modeled. The

selection approach is discussed further in Section 5.1.

1

See www.energycodes.gov/development/commercial/90.1_models.

2.3

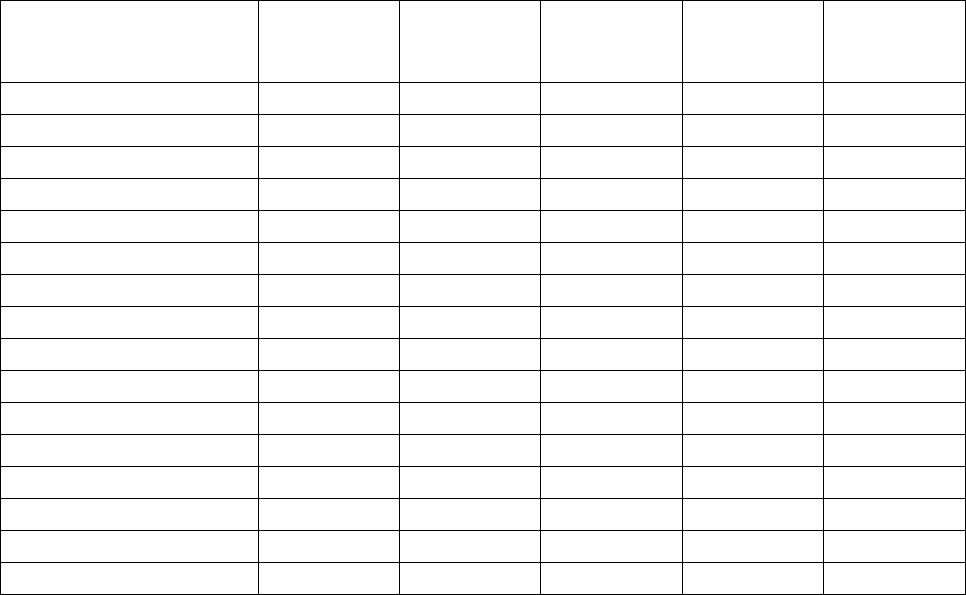

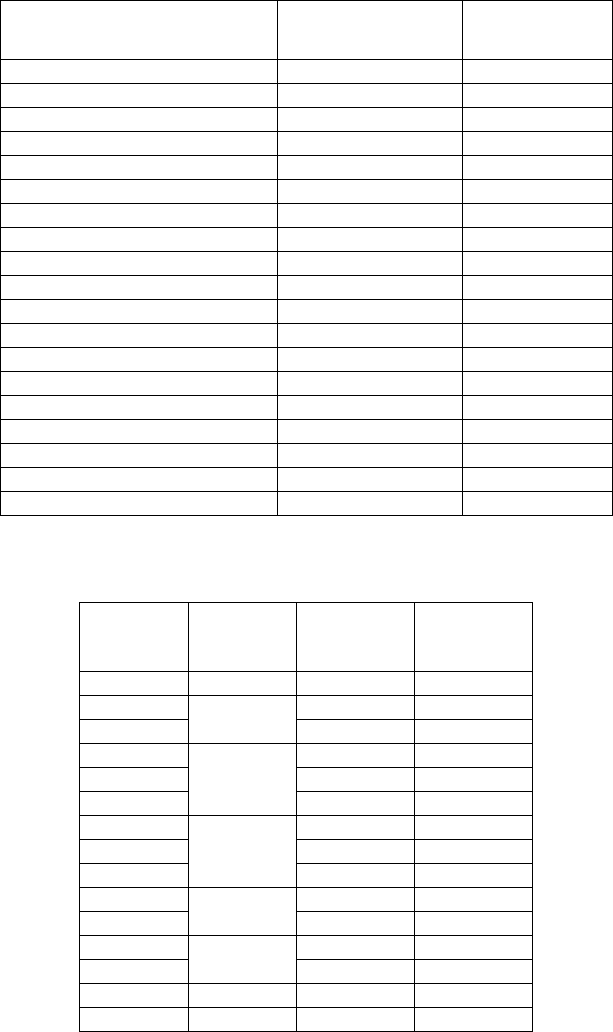

Table 2.1. Commercial Prototype Building Basic Characteristics

Building Prototype

Floor Area

(ft²)

Number of

Floors Aspect Ratio

Window-to-

Wall Ratio

(WWR)

Floor-to-

Floor Height

(ft)

Small Office 5,500 1 1.5 15% 10

Medium Office 53,630 3 1.5 33% 13

Large Office 498,640 12* 1.5 40% 13

Standalone Retail 24,690 1 1.28 7% 20

Strip Mall 22,500 1 4 11% 17

Primary School 73,970 1 N/A 35% 13

Secondary School 210,910 2 N/A 33% 13

Outpatient Healthcare 40,950 3 N/A 20% 10

Hospital 241,410 5* 1.33 16% 14

Small Hotel 43,210 4 3 11% 9, 11

‡

Large Hotel 122,120 6* 5.1, 3.8** 27% 10, 13

‡

Warehouse 52,050 1 2.2 0.71%

†

28

Quick-Service Restaurant 2,500 1 1 14% 10

Full-Service Restaurant 5,500 1 1 18% 10

Mid-Rise Apartment 33,740 4 2.75 15% 10

High-Rise Apartment 84,360 10 2.75 15% 10

* These buildings also include a basement, which is not included in the number of floors.

** The large hotel basement aspect ratio is 3.8:1; all other floors have an aspect ratio of 5.1:1.

† For the warehouse, 0.71% is the overall WWR. The warehouse area has no windows; the WWR for the small office in the

warehouse is 12%.

‡ The second number is the height of the first floor only.

2.1.3 Default Inputs

Input values for building components that do not differ between the two subject codes will be set to

either 1) match a shared code requirement if one exists, 2) match standard reference design specifications

from the code’s performance path if the component has such specifications, or 3) match best estimates of

typical practice otherwise. Examples of these items are 1) wall insulation R-values that are the same in

both code editions, 2) the heating system type required for performance analysis, and 3) typical internal

equipment (plug) loads based on surveys or load calculation handbooks, respectively. Because such

component inputs are used in both pre- and post-revision simulations, their specific values are considered

neutral and are of secondary importance, so it is important only that they be reasonably typical of the

construction types being evaluated.

2.4

2.1.4 Provisions Requiring Special Consideration

Some building components or energy conservation measures do not lend themselves to

straightforward pre- and post-change simulation of energy consumption. For example, the use of hourly

simulation is of dubious value in assessing the energy impact of service water heat piping insulation.

Rather than including an exact piping heat loss model in the building simulation, typical expected losses

may be separately calculated and entered as loads into the simulation model.

Another situation requiring special consideration involves analysis of new or innovative equipment

that cannot be implemented directly in the energy simulation software. One example is a heat recovery

device for service water heating that uses heat rejected from the chiller. Analysis of such a proposal can

be effectively performed by analyzing the load outputs from EnergyPlus in a separate tabular analysis

using standard engineering formulas for the impact of heat recovery on the energy use of the building.

Another example of post processing is analysis of water-side economizers for Addendum du to ASHRAE

Standard 90.1-2013 using hourly data extracted from EnergyPlus models (Hart et al. 2014a).

2.2 Weather Locations

Simulations (and other analyses as appropriate) will usually be conducted in one representative

weather location per selected climate zone in the code, including a separate location for each moisture

regime.

2

Table 2.2 shows the climate locations typically used for a national savings analysis, each of

which is represented by a Typical Meteorological Year (TMY3)

3

weather data file. The locations shown

in Table 2.2 for analysis through Standard 90.1-2013 were selected to be reasonably representative of

their respective climate zones by Briggs et al. (2003). ASHRAE SSPC 90.1 has recently updated the

representative cities to adopt changes made in ASHRAE Standard 169-2013, Climatic Data for Building

Design Standards, and to provide a better match for actual average climate in each climate zone. DOE

may use these updated representative locations (also shown in Table 2.2) for analysis starting with

Standard 90.1-2016 and the 2018 IECC. There are several approaches for climate zone selection:

• For a national level energy saving analysis, up to 16 climate locations are used, selected from those

shown in Table 2.2.

• For a national level cost-effectiveness analysis, DOE may select a subset of the climate zones to

represent most of the energy and cost impacts of the code changes in a particular code or proposal

analysis. The selection approach is discussed further in Section 5.1.

• For a state level code cost-effectiveness analysis, alternate cities located in each climate zone for the

state are selected. A TMY3 weather station with robust data is selected within the state where

possible, or adjacent to the state being analyzed if better data is in the adjacent city.

• For measures or code changes that impact primarily building envelope or are not impacted by

humidity conditions, the cities representing the thermal climate zones may be used, with the results

applying to the climate zones that share the same thermal climate zone numbers, regardless of

moisture regime.

2

Moisture regimes reflect the average humidity in a climate zone. As seen in Table 2.2, moisture regime A

represents higher humidity (moist) than B (dry), while marine (C) zones have some moisture, but also have more

moderate temperature ranges.

3

See http://rredc.nrel.gov/solar/old_data/nsrdb/1991-2005/tmy3/ .

2.5

• Some analyses are conducted only for the adjoining climate zones where requirements are proposed

to change. For example, increased exterior duct insulation in climate zone 5 and colder only requires

an analysis in thermal climate zones 4 and 5 where the analysis shows the extra insulation is not cost-

effective in climate zone 4, but is cost-effective in climate zone 5. Because a logical argument can be

made that colder climate zones will result in more heat loss, the extra insulation can be presumed to

be cost-effective in climate zones 6 through 8.

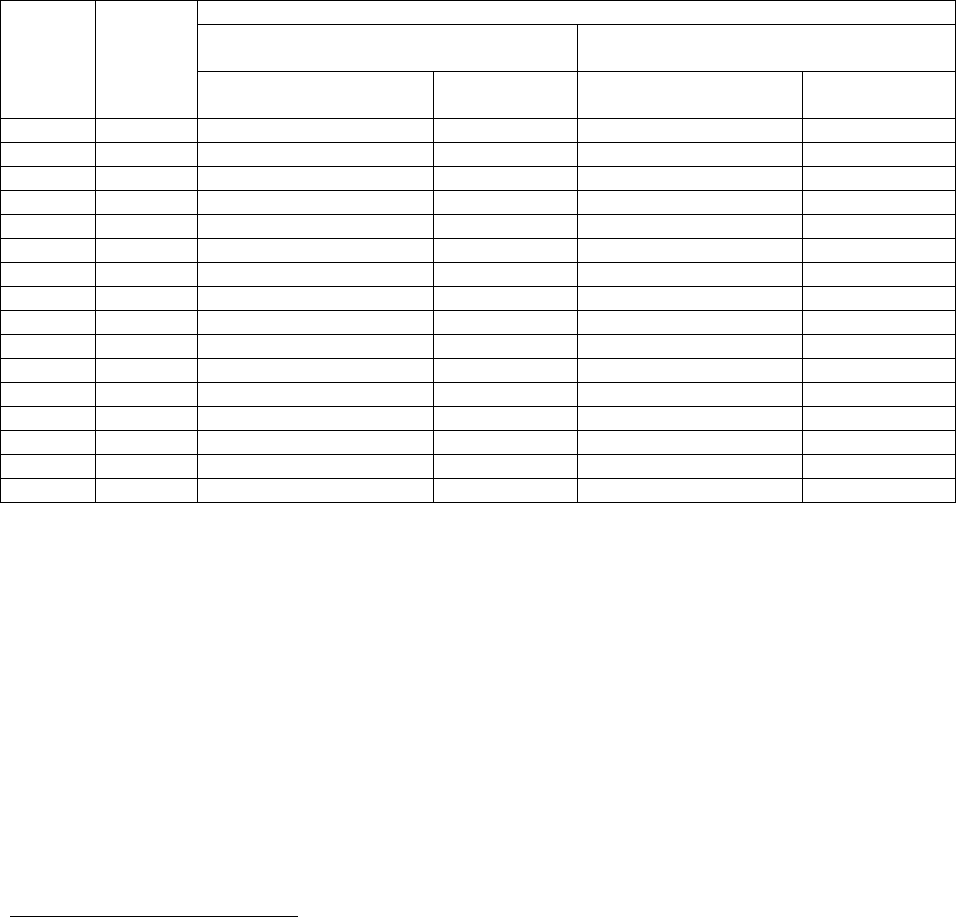

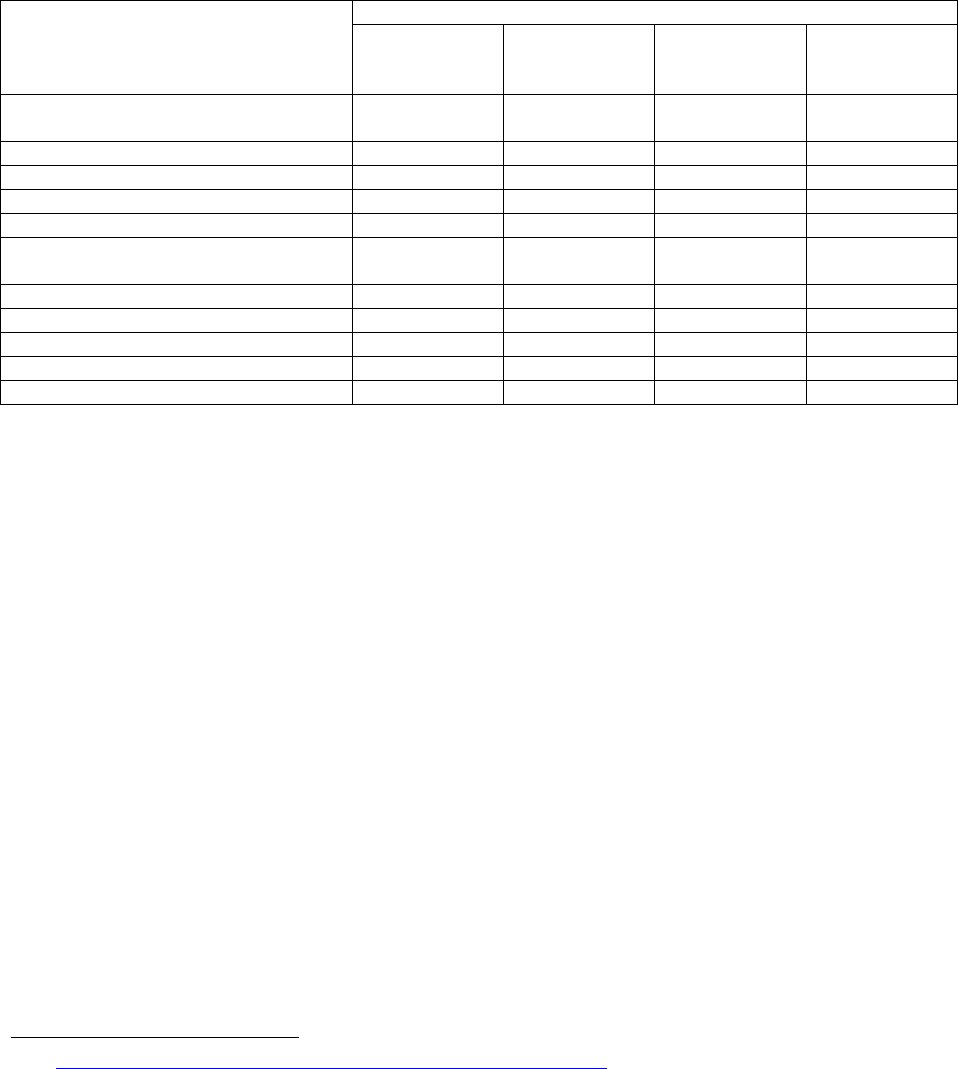

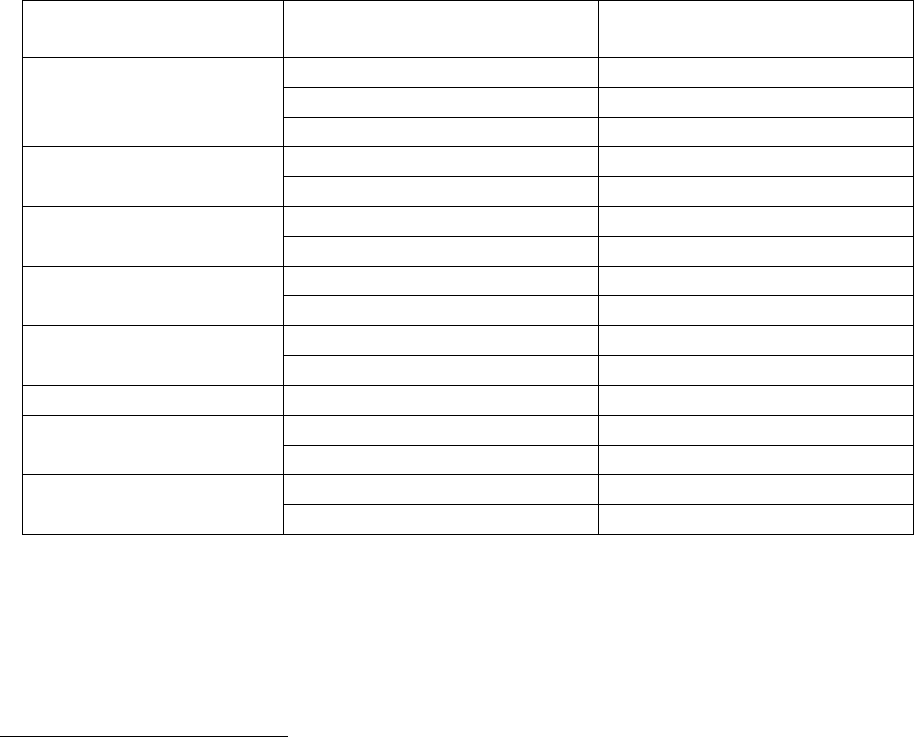

Table 2.2. Climate Locations Used in Energy Simulations

Climate

Zone*

Moisture

Regime

Representative Locations for 90.1 National Analyses

Analysis Before and Including 90.1-2013

and 2015 IECC

Analysis Starting with 90.1-2016 and

2018 IECC

City, State

Thermal

Climate Zone

City, State

Thermal

Climate Zone

1A

Moist

Miami, FL

1

Honolulu, HI

1

2A

Moist

Houston, TX

2

Tampa, FL

2

2B

Dry

Phoenix, AZ

N/A

Tucson, AZ

N/A

3A

Moist

Memphis, TN

N/A

Atlanta, GA

3

3B

Dry

El Paso, TX

3

El Paso, TX

N/A

3C

Marine

San Francisco, CA

N/A

San Diego, CA

N/A

4A

Moist

Baltimore, MD

N/A

New York, NY

4

4B

Dry

Albuquerque, NM

4

Albuquerque, NM

N/A

4C

Marine

Salem, OR

N/A

Seattle, WA

N/A

5A

Moist

Chicago, IL

5

Buffalo, NY

5

5B

Dry

Boise, ID

N/A

Denver, CO

N/A

5C

Marine

n/a

N/A

Port Angeles, WA

N/A

6A

Moist

Burlington, VT

6

Rochester, MN

6

6B

Dry

Helena, MT

N/A

Great Falls, MT

N/A

7

N/A

Duluth, MN

7

International Falls, MN

7

8

N/A

Fairbanks, AK

8

Fairbanks, AK

8

* Climate zones outside the United States are not shown.

2.3 Energy Cost Savings

Annual energy costs are a necessary part of the cost-effectiveness analysis. They are based on the

energy consumption multiplied by average energy prices. For the national Standard 90.1 analysis, DOE

will use the same energy prices as approved by ASHRAE SSPC 90.1 for standard development—energy

prices that were based on DOE Energy Information Administration (EIA) data. Using the same prices

that were used for development of a particular edition of Standard 90.1 provides a consistent approach

and applies a similar cost-effectiveness threshold to the entire standard that was used for individual

proposals as the standard was developed. The ASHRAE 90.1 Scalar Method identifies a fossil fuel rate

4

that is primarily applied to heating energy use, with some application to service water heating. DOE may

apply this mixed fuel approach to state cost-effectiveness analysis.

4

The ASHRAE 90.1 Scalar Method fossil fuel rate is a blended heating rate and includes proportional costs for

natural gas, propane, heating oil, and electric heat relative to national heating fuel use share. Heating energy use in

the prototypes for fossil fuel equipment is calculated in therms based on natural gas equipment, but in practice,

similar equipment may be operated on propane, or boilers that are modeled as natural gas may use oil in some

regions.

2.6

In any event, prices used for cost-effectiveness energy analyses are derived from the DOE EIA data

(EIA 2012, 2014). DOE intends to use the most recently available national or state annual average

commercial energy prices from the EIA. Annual average prices are used to avoid selecting a short-term

price that is subject to seasonal fluctuations. If energy prices from the most recent year(s) are unusually

high or low, DOE may use a longer-term average of energy prices, such as the average from the past 3

years and projections for the next 2 years.

5

For individual state analysis, DOE intends to use state annual

average commercial energy prices from EIA. The energy prices used in a specific analysis along with

their source will be declared and documented in that analysis.

5

EIA energy projections are available from either the Short-Term Energy Outlook or Annual Energy Outlook

3.1

3.0 Estimating the Incremental Costs of Code Changes

The second step in assessing the cost-effectiveness of a proposed code change or a newly revised

code is estimating the first cost of the changed provision(s). The first cost of a code change refers to the

marginal cost of implementing one or more changed code provisions. For DOE’s analyses, first cost

refers to the retail cost (the total cost to a building developer) prior to amortizing the cost over multiple

years through financing, and includes the full price paid by the building developer, including materials,

sales taxes, labor, overhead, and profit. First cost excludes maintenance and other ongoing costs

associated with the new code provision(s). Where regular maintenance costs are expected to be

significantly different as a result of code requirements, they are estimated and converted to an annual

maintenance cost, then accounted for separately on an annualized basis in the LCC calculation. There are

also replacement costs estimated when individual component life is shorter than the economic study

period.

DOE recognizes that estimating the first cost of a code change can be challenging, and will attempt to

identify credible cost estimates from multiple sources when possible. Judgment is often required to

determine an appropriate cost for energy code analysis when multiple credible sources of construction

cost data yield a range of first costs. Cost data will be obtained from existing sources, including cost

estimating publications such as RS Means cost estimating handbooks

1

; industry sources (often through

web sites); and other resources including journal articles, research, and case studies. DOE may also

subcontract with engineering or architectural professionals to provide specialized expertise and complete

cost estimates for energy efficiency measures or representative building systems. DOE will use all of

these resources to determine the most appropriate construction cost parameters based on factors including

the applicability and thoroughness of the data source.

3.1 Cost Estimating Approach

The first step in developing the incremental cost estimates is to define the items to be estimated, such

as specific pieces of equipment and their installation. The second step begins by defining the types of

costs to be collected. Cost estimates cover incremental costs for material, labor, construction equipment,

commissioning, maintenance, and overhead and profit. These costs are estimated both for initial

construction and for replacing equipment or components at the end of their useful life during the study

period. The third step is to compile the unit and assembly costs needed for the cost estimates. These

costs are derived from multiple sources:

• Cost estimating consulting firms; mechanical, electrical, and plumbing (MEP) consulting engineering

firms; or specialized consultants (such as daylighting) may be retained to develop general cost

estimates applicable to code changes in the prototypes.

• Cost estimates for new work and later replacements are developed to approximate what a general

contractor typically submits to the developer or owner and include subcontractor and contractor costs

and markups.

1

RS Means cost estimating handbooks are available at www.rsmeans.com/.

3.2

• Maintenance costs are intended to reflect what a maintenance firm would charge. Once initial costs

are developed, a technical review is often conducted by members of the ASHRAE SSPC 90.1 and

PNNL internal sources.

3.2 Sources of Cost Estimates

Table 3.1 describes typical sources of cost estimates by category. This table is an example based on

the national cost-effectiveness analysis of Standard 90.1-2013 (Hart et al. 2014b), and is typical of

sources of costs that will be used in completing cost-effectiveness analyses of codes and efficiency

standards for commercial buildings. In this example, RS Means refers to any of the appropriate RS

Means cost estimating handbooks.

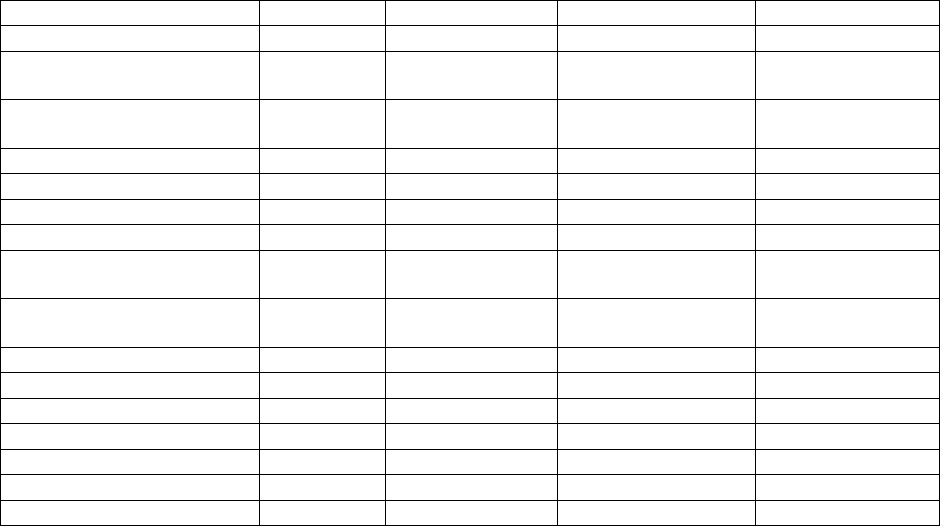

Table 3.1. Example Sources of Cost Estimates by Cost Category

Cost Category

Typical Sources

HVAC

Motors included in this category

Cost estimator and PNNL staff used quotes from suppliers and

manufacturers, online sources, and their own experience.*

HVAC

Ductwork, piping, selected controls

items

MEP consulting engineers provided ductwork and plumbing costs based on

one-line diagrams they created as well as the model outputs, including

system airflows, capacity, and other factors, and provided detailed costs by

duct and piping components using RS Means 2012. The MEP consulting

engineers also provided costs for several control items.*

HVAC

Selected items

PNNL used internal expertise and experience supplemented with online

sources.*

Lighting

Interior lighting power allowance and

occupancy sensors

PNNL staff with input from ASHRAE 90.1 Lighting Subcommittee.

Product catalogs were used for consistency with some other online sources

where needed.

Lighting

Daylighting

PNNL staff and daylighting consulting firm.

Envelope

Opaque insulation and fenestration

Costs dataset developed by professional cost estimator.*

Commissioning

Cost estimator, RS Means 2014, MEP consulting engineers, and PNNL

staff expertise.

Labor

RS Means 2014 and the MEP consulting engineers for commissioning rate.

Replacement life

Lighting equipment including lamps and ballasts from product catalogs.

Mechanical from ASHRAE 90.1 Mechanical Subcommittee protocol for

cost analysis.

Maintenance

Originator of the other costs for the affected items, or PNNL staff expertise.

* Where detailed costs were developed in 2012, they were updated to 2014 using inflation factors developed from RS Means

handbooks, as discussed in Section 3.4.

3.2.1 Approach to Cost Data Collection

For code changes that impact many system or construction assembly elements of a building, DOE

consults multiple national construction cost estimation publications published by RS Means, which

provide a wide variety of construction cost data. This is appropriate for many code changes that impact

3.3

the construction of commercial buildings (e.g., increasing insulation thickness on piping) where the

efficiency change can be tied to incremental changes in material thickness or items clearly identified in

the estimating guides. RS Means cost handbooks do not always identify the efficiency levels of products

and may not have both standard and high-efficiency options. They do not, for example, have detailed

costs on improved duct sealing or building envelope sealing, and the costs for fenestration products

(windows, doors, and skylights) are focused on aesthetic features rather than energy efficiency

characteristics such as solar heat gain coefficient or low-e coatings.

When a code change impacts only the materials used in a building, without impacting labor, cost data

can often be obtained from national suppliers. These sources can have the advantage of providing recent

costs, and the costs can be localized if a state or local analysis is needed. However, these sources often do

not provide all the specific energy efficiency measure improvements that are typically needed for code

improvement analyses.

As needed, DOE conducts literature searches of specialized building science research publications

that assess the costs of new or esoteric efficiency measures that are not covered in other data sources.

Examples include energy efficiency case studies, surveys of demonstration projects, utility or regional

energy economic potential savings studies, and journal articles.

3.2.2 Economies of Scale and Market Transformation Effects

Construction costs often show substantial differences between regions, sometimes based primarily on

local preferences and the associated economies of scale. Because new code changes may require building

construction with new and potentially unfamiliar techniques in some locations, initial local cost estimates

may overstate the long-term costs of implementing the change. For example, economizer fault

diagnostics or LED parking lot lighting may be reasonably priced in California, where the technology has

been required by code for a period of time. In southeastern states, the price for the same technology may

be high, due to contractor unfamiliarity. Similar issues may arise where manufacturers produce large

quantities of a product that just meet a current energy code requirement, giving that product a relatively

low price in the market. Should the code requirement increase, it is likely that manufacturers will

increase production of a new conforming product, lowering its price relative to the current premium for

what is now a high efficiency product.

DOE intends to evaluate new code changes case by case to determine whether it is appropriate to

adjust current costs for anticipated market transformation after a new code takes effect. DOE intends to

evaluate specific new or proposed code provisions to determine whether and how prices might be

expected to follow an experience curve with the passage of time. It is noted that site-built construction

may involve several types of efficiency improvements. The real cost of code changes requiring new

technologies may drop in the future as manufacturers learn to produce them more efficiently. The long-

term cost of code changes that involve new techniques may likewise drop as contractors learn to

implement them in the field more efficiently and with less labor. Finally, code changes that simply

require more of a currently used technology or technique may have relatively stable real costs, with prices

generally following inflation over time.

3.4

3.2.3 Addressing Code Changes with Multiple Approaches to Compliance

One challenge of estimating the costs of energy code changes is selecting an appropriate

characterization of new code requirements. A requirement for lower fan horsepower, for example, might

be met with a more efficient fan, high surface area filters, better belts, a premium efficiency motor, more

but smaller fan units, larger ductwork, or some combination of these options. Each approach will have

different costs and may be subject to differing constraints depending on the situation. Some approaches,

for example, may be inappropriate in some building types, but not others. Some approaches may open the

possibility for new and less expensive construction approaches. Overall, DOE intends to apply two

principles in reviewing options in the code:

• A single option will be selected for analysis that is expected to be the least-cost method of compliance

that is considered to represent typical construction.

• If a requirement includes multiple options, and one analyzed option that is widely applicable is found

to be cost-effective, the requirement will be deemed cost-effective. It is not necessary to demonstrate

the cost-effectiveness of all options. This is because there is a cost-effective path through the code,

and if a higher cost option is chosen, that is the developer or designer’s choice.

It is difficult for DOE to anticipate either the types of code changes that will emerge in future

building energy codes or the manner in which developers will choose to meet the new requirements;

however, DOE intends to evaluate changes case by case and seek the least-cost way to achieve

compliance unless that approach is deemed inappropriate in a large percentage of situations. For code

changes that touch on techniques with which there is recent research experience (e.g., through DOE’s

Federal Energy Management Program (FEMP)

2

and Building Technologies Office

3

), DOE will consult

the relevant publications or researchers for advice on appropriate construction assumptions.

DOE anticipates that some new code provisions may have significantly different first costs depending

on unrelated aesthetic choices or exceptions and flexibility options in the code. For example, a

requirement for window shading could be met with interior blinds, electrochromatic windows, static

exterior shading devices, or an active tracking exterior shading system. In addition, optional trade-offs

may be included in the code that guarantee minimum energy performance but are not necessarily

evaluated for cost-effectiveness. For example, a maximum window-to-wall ratio may be established as a

baseline, but a predetermined trade-off may allow the building design to exceed that ratio if an energy

recovery device or other energy saving options are included. Because the additional windows and energy

saving options are optional, it is not necessary to establish the cost-effectiveness of the alternative design

combination.

Finally, some new code provisions may come with no specific construction changes at all, but rather

be expressed purely as a performance requirement. It is also conceivable that a code could be expressed

simply as energy use intensity, where the requirement is a limit on energy use per square foot of

conditioned floor area. DOE intends to evaluate any such code changes case by case and will conduct

literature research or new analyses to determine the reasonable set of construction changes that could be

expected to emerge in response to such new requirements. Again, DOE intends to focus on the least-cost

approach deemed to be reasonable, cost-effective, and meet the code requirement.

2

See http://energy.gov/eere/femp/articles/technologies.

3

See http://energy.gov/eere/buildings/improving-energy-efficiency-commercial-buildings.

3.5

3.3 Cost Parameters

Several general parameters are typically applied to all of the cost estimates. These items include new

construction material and labor cost adjustments, a replacement labor hour adjustment, replacement

material and labor cost adjustments, and a project cost adjustment. The cost adjustments were developed

by PNNL during the cost-effectiveness analysis of Standard 90.1-2010 and were based on cost-estimating

guides and practices of cost-estimating consultants for that study (Thornton et al. 2013). DOE intends to

use these parameters for future estimates—unless there are changes noted in the industry—and they are

described in Table 3.2.

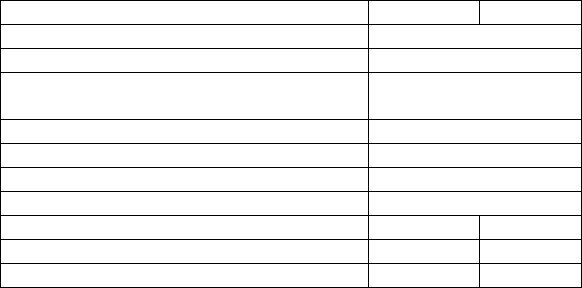

Table 3.2. Cost Estimate Adjustment Parameters

Cost Items

Value*

Description**

New construction labor cost

adjustment

52.6%

Labor costs used are base wages with fringe benefits. Added to this is

19%: 16% for payroll, taxes, and insurance including worker's

compensation, Federal Insurance Contributions Act, unemployment

compensation, and contractor’s liability, and 3% for small tools. The

labor cost plus 19% is multiplied by 25%: 15% for home office

overhead, and 10% for profit. A contingency of 2.56% is added as an

allowance to cover wage increases resulting from new labor agreements.

New construction material

cost adjustment

15.0%

to

26.5%

Material costs are adjusted for a waste allowance set at 10% in most

cases for building envelope materials. For other materials such as HVAC

equipment, 0% waste is the basis. The material costs plus any waste

allowance are multiplied by the sum of 10% profit on materials, and sales

taxes. An average value for sales taxes of 5% is applied.

Replacement - additional

labor allowance

65.0%

Added labor hours for replacement to cover demolition, protection,

logistics, cleanup, and lost productivity relative to new construction.

Added prior to calculating replacement labor cost adjustment.

Replacement labor cost

adjustment

62.3%

The replacement labor cost adjustment is used instead of the new

construction labor cost adjustment for replacement costs. The adjustment

is the same except for subcontractor (home office) overhead, which is

23% instead of 15% to support small repair and replacement jobs.

Replacement material cost

adjustment

26.5%

to

38.0%

The replacement material cost adjustment is used instead of the new

construction material cost adjustment for replacement costs. The

adjustment is for purchase of smaller lots and replacement parts. 10% is

added and then is adjusted for profit and sales taxes.

Project cost adjustment

28.8%

The combined labor, material, and any incremental commissioning or

construction costs are added together and adjusted for subcontractor

general conditions and for general contractor overhead and profit.

Subcontractor general conditions add 12% and include project

management, job-site expenses, equipment rental, and other items. A

general contractor markup of 10% and a 5% contingency are added to the

subcontractor subtotal as an alternative to calculating detailed general

contractor costs (RS Means 2014).

* Values shown and used are rounded to first decimal place.

** Values provided by the cost estimator except where noted.

For national cost-effectiveness studies, costs are not adjusted for climate locations. The climate

location results are intended to represent an entire climate subzone even though climate data for a

particular city is used for simulation purposes. Costs will vary significantly between a range of urban,

suburban, and rural areas within the selected climate locations, which typically cross multiple states. For

state-level cost-effectiveness analysis, costs are adjusted for specific cities based on city cost index

adjustments from RS Means or other sources.

3.6

3.4 Cost Updating for Inflation

Cost estimates are typically developed for current national average prices. Labor costs are based on

estimated hours and current crew labor rates from RS Means. In some cases, cost estimates completed for

a prior code cycle are still applicable, and are adjusted for inflation rather than creating a new cost

estimate or obtaining current unit prices throughout the cost estimate. Where cost estimates are updated,

inflation factors specific to the equipment are used. These inflation factors are developed for each

specific equipment or insulation type by comparing RS Means from the time of the estimate with the

current RS Means.

3.5 Cost Estimate Spreadsheet Workbook

To provide a transparent view of the costs used in the analysis, a cost estimate spreadsheet will

typically be prepared in conjunction with the cost-effectiveness report. The intent of such a cost estimate

is to show the basis for costs used in the analysis, although in some cases detailed information obtained

from individual manufacturers will be averaged and only the average value will be included in the

documentation. For some individual proposals, a spreadsheet may not be necessary, as the costs may be

cited from other documents or sources. As one example, the cost estimate spreadsheet for the analysis of

Standard 90.1-2013 (Hart et al. 2014b) was organized in the following sections:

1. Introduction

2. HVAC cost estimates

3. Lighting cost estimates

a. Interior lighting power density

b. Interior lighting occupancy related controls

c. Daylighting controls

4. Envelope, power, and other cost estimates

5. Cost estimate summaries and cost-effectiveness analysis results

DOE may also provide a calculating tool that allows cost adjustments to be entered, especially for

state analysis. This allows local evaluation of particular cost or other economic impacts to be adjusted in

evaluating codes for use by states in the adoption process. For DOE’s assessment of cost-effectiveness,

the researched input values for economic and cost parameters will continue to be used.

4.1

4.0 Estimating the Cost-effectiveness of Code Changes

The last step in assessing the cost-effectiveness of a proposed code change or a newly revised code is

calculating the corresponding economic impacts of the changed provision(s). These impacts are

measured under different economic scenarios with several economic metrics.

4.1 Cost-effectiveness Analysis

The intent of the DOE cost-effectiveness methodology is to determine whether code changes are

economically justified from the perspective of a public policy that balances increased building costs

against energy savings over time. The DOE methodology accounts for the benefits of energy-efficient

building construction to building owners and tenants that accrue over 30 years. To accommodate

multiple economic views, the LCC analysis is applied to multiple scenario methods: Publicly-Owned

Method, Privately-Owned Method, and ASHRAE 90.1 Scalar Method. The scenarios, methodologies,

and input parameters are described in this section.

Cost-effectiveness is analyzed using the incremental cost information presented in Section 3.0 and the

energy cost information presented in Section 2.0. Multiple economic metrics are available, as discussed

further in Section 4.2. Several of these may be presented in a particular analysis, and they are selected

from the following:

• Life-cycle cost net savings (a.k.a., NPV of savings)

• Savings-to-investment ratio

• The ASHRAE 90.1 scalar ratio

• Simple payback period

4.1.1 Economic Scenarios

Commercial building developers and owners have different perspectives, depending primarily on

whether the ownership is public or private. The building owner has a different view of the economic

impact of energy purchases as a landlord than as an owner who occupies the building. In tenant

situations, the energy operating costs may be paid by the tenant directly to utilities or indirectly via the

building owner through a net lease. In the latter situation, the costs for energy efficiency may be paid by

a building owner who does not receive energy benefits through reduced bills; however, these incremental

costs can be considered to be passed through to the tenant in the lease rates. In every case, someone will

pay the energy bill for the building—having savings if it is a more efficient building—and someone will

pay the added cost of a more efficient building. While local rental market conditions may result in higher

or lower lease rates relative to the incremental cost of efficiency improvements, a complete economic

model of such variability would be quite difficult to implement. To provide a straightforward and

economic equivalent analysis, the cost-effectiveness analysis will be from the point of view of a building

owner who receives the benefits of energy savings. This approach puts the analysis of the costs and

savings of all energy saving measures on a common footing for analysis.

4.2

DOE evaluates energy codes and code proposals based on LCC analysis over a multi-year study

period, accounting for energy savings, incremental investment for energy efficiency measures, and other

economic impacts. The value of future savings and costs are discounted to a present value, with

improvements deemed cost-effective when the NPV of savings (present value of savings minus present

value of costs) is positive. Because the economic criteria of different commercial building owners vary,

up to three scenarios may be used for cost-effective analysis:

• Scenario 1 (also referred to as the Publicly-Owned Method): LCC analysis method representing

government or public ownership (without borrowing or taxes). This scenario uses a real dollar

methodology and economic inputs that have been established for federal projects under FEMP as

amended by the Energy Independence and Security Act of 2007 (EISA).

• Scenario 2 (also referred to as the Privately-Owned Method): LCC analysis method representing

private or business ownership (includes loan and tax impacts). This scenario uses typical commercial

economic inputs, with initial costs being financed, and considers tax impacts for savings, interest, and

depreciation. The general methodology is identical to that used under Scenario 1, except that it is a

nominal dollar analysis with the addition of consideration for income and property taxes, financing,

and a private sector discount rate.

• Scenario 3 (also referred to as the ASHRAE 90.1 Scalar Method (McBride 1995)): Represents a pre-

tax private investment point of view, and uses economic inputs established by the ASHRAE SSPC

90.1. The ASHRAE 90.1 Scalar Method uses standard life-cycle costing techniques in a similar

manner to Scenarios 1 and 2, although the parameters and methodology used in the analysis are

established by ASHRAE SSPC 90.1.

It is important to understand that, except for the minor adjustments noted here, DOE uses methods

and parameters established by others for Scenarios 1 and 3. Scenario 1 parameters are established by

federal statute (42 U.S.C. 8254). Scenario 3 parameters are established by ASHRAE SSPC 90.1 for each

edition of Standard 90.1. The method and parameters used for Scenario 2 are established by DOE,

although the method and parameters are developed and selected to be consistent with Scenario 1 except

where typical private investment criteria support different parameters.

When selecting scenarios for a particular cost-effectiveness analysis, DOE notes that Scenarios 2 and

3 both reflect a private-ownership view. As a result, each analysis typically includes Scenario 1 to reflect

a public-ownership view and the private-ownership view is reflected by either Scenario 2 or 3. For a

national analysis, the ASHRAE Scalar Method (McBride 1995) is used for the private-ownership view, as

this was the method applied to individual proposals in development of the standard. The ASHRAE

energy prices are typically used for the national analysis, again for consistency with the individual

proposal analyses. For individual state analysis, DOE typically uses local state energy prices, and cost-

effectiveness is determined based on LCC using Scenario 1 and Scenario 2 economic parameters.

Scenario 2 is used as the Private-Ownership Method for state analysis, since the method and parameter

selection can be maintained on a consistent basis by DOE. Scenario 2 also more closely matches

Scenario 1 and the cost-effectiveness method used for residential codes than does Scenario 3.

4.1.2 Cost-effectiveness Methodology

The primary basis of cost-effectiveness assessment is an LCC analysis. The LCC analysis

perspective compares the present value of incremental costs, replacement costs, and maintenance and

4.3

energy cost savings for each prototype building and climate location. The degree of borrowing and the

impact of taxes vary considerably for different building projects, creating many possible cost scenarios.

These varying costs are not included in the Scenario 1 Publicly-Owned Method LCC analysis, but are

included with the Privately-Owned Method Scenario 2 analysis and the Scenario 3 SSPC 90.1 Scalar

Method.

The LCC analysis approach is based on the LCC analysis method used by FEMP,

1

a method required

for federal projects and used by other organizations in both the public and private sectors (NIST 1995).

The LCC analysis method consists of identifying costs (and revenues, if any) and the year in which they

occur, and determining their value in present dollars (known as the net present value). This method uses

fundamental engineering economics relationships about the time value of money. For example, money in

hand today is normally worth more than money received tomorrow, which is why people pay interest on a

loan and earn interest on savings. Future costs are discounted to the present based on a discount rate. The

discount rate may reflect what interest rate can be earned on other conventional investments with similar

risk, or in some cases, the interest rate at which money can be borrowed for projects with the same level

of risk.

4.1.2.1 Discounted Value

The following calculation method can be used to account for the present value of costs or revenues:

Present Value = Future Value

/ (1+ i)

n

i is the discount rate (or interest rate in some analyses)

n is the number of years in the future the cost occurs

The present value of any cost that occurs at the beginning of year 1 of an analysis period is equal to

that initial cost. For this analysis, initial construction costs occur at the beginning of year 1, and all

subsequent costs occur at the end of the future year identified.

4.1.2.2 Study Period

The LCC analysis depends on the number of years into the future that costs and revenues are

considered, known as the study period. While the FEMP method allows a 40-year

2

study period (42

U.S.C. 8254(a)(1)),

the DOE code analysis method uses 30 years for Scenarios 1 and 2 and 40 years for

Scenario 3. Thirty years is the same study period used for the cost-effectiveness analysis of the

residential energy code, conducted by DOE and PNNL (DOE 2012), and is the same period used in

previous cost-effectiveness evaluations of Standard 90.1 (Thornton et al. 2013; Hart et al. 2014a).

National Institute of Standards and Technology (NIST)-provided energy escalation and discount rates are

also limited to 30 years. The 30-year study period is also widely used for LCC analysis in government

and industry, and the

Office of Management and Budget long-term study period is set at 30 years. The

study period is also a balance between capturing the impact of future replacement costs, inflation, and

energy escalation; the higher the uncertainty of these costs, the further into the future they are considered.

1

See 10 CFR part 436, subpart A, “Methodology and Procedures for Life Cycle Cost Analyses,” Jan. 1, 2004.

2

Section 441 of EISA amended the FEMP cost-effective methodology to increase the maximum study period from

25 to 40 years (42 U.S.C. 8254(a)(1)).

4.4

4.1.2.3 Residual Value

When the length of the study period does not exactly match the measure life, the residual value of

equipment beyond the period of analysis is accounted for. The FEMP LCC analysis method includes a

simplified approach for determining the residual value. The residual value is the proportion of the initial

cost equal to the remaining years of service divided by the initial cost. For example, the residual value of

a wall assembly in year 30 is (40-30)/40 or 25% of the initial cost. The residual values applied in year 30

are discounted from year 30 to a present value and included as a reduction in the total present value of

cost. Three cases need to be considered for residual value:

• Where the measure life matches the study period, or an even multiple of the life matches the study

period, there is no residual value. For example, electronic controls with a 15-year life in a 30-year

study period include a replacement cost at year 15, and that replacement has no further value at year

30, so the residual value is zero.

• Where the useful life of equipment or materials extends beyond the study period, there is a residual

value. For code measures analyzed, the longest useful life defined is 40 years for all envelope cost

items, such as wall assemblies, as recommended by the SSPC 90.1 Envelope Subcommittee. Forty

years is longer than the 30-year study period used in Scenario 1 and 2 LCC analyses. A residual

value of the unused life of a cost item is calculated at the last year of the study period for components

with longer lives than the study period. So, for example, a measure with a 40-year life in a 30-year

study period would have a residual value of 25% of its first cost.

• Where the replacement life does not fit neatly into the study period (e.g., a chiller with a 23-year

useful life), the residual value is not a salvage value, but rather a measure of the available additional

years of service not yet used for the replacement. To use the chiller example with a 30-year study

period, at 30 years there is a 16-year (23+23-30) residual life remaining. So the residual value would

be (46-30)/23, or 69.5% of the replacement cost, discounted from year 30 to present value.

4.2 Economic Metrics

In evaluating code change proposals and assessing new editions of commercial building energy

codes, DOE intends to calculate multiple metrics selected from the following:

• Life-cycle cost net savings (a.k.a., NPV of savings)

• Savings-to-investment ratio

• The SSPC 90.1 scalar ratio

• Simple payback period

Life-cycle cost net savings is the primary metric DOE intends to use to evaluate whether a particular

code change is cost-effective. Any code change that results in an LCC net savings greater than or equal to

zero (i.e., monetary benefits exceed costs) will be considered cost-effective. The payback period and SIR

analyses provide additional information DOE believes is helpful to other participants in code change

processes and to states and jurisdictions considering adoption of new codes. These metrics are discussed

further below.

4.5

4.2.1 Life-Cycle Cost Net Savings

Life-cycle cost net savings is a robust cost-benefit metric that sums the costs and benefits of a code

change over a specified period. Sometimes referred to as net present value analysis or engineering

economics, LCC analysis is a well-known approach to assessing cost-effectiveness. Because the key

feature of LCC analysis is the summing of costs and benefits over multiple years, it requires that cash

flows in different years be adjusted to a common year for comparison. This is done with a discount rate

that accounts for the time value of money. Like most LCC implementations, DOE’s method sums cash

flows in year-zero dollars, which allows the use of standard discounting formulas. Cash flows adjusted to

year zero are termed present values. The procedure used for discounting is taken directly from the FEMP

cost-effective methodology for federal buildings

3

as described in NIST Handbook 135 (Fuller and

Petersen 1995). In actual practice, these procedures have been implemented in a spreadsheet format to

produce identical results, rather than using the manual worksheets included in NIST Handbook 135 or the

FEMP Building Life Cycle Cost computer program.

4

Formulas shown in Table 4.4 are taken from or

adapted directly from formulas in NIST Handbook 135. Where situations are not covered by the FEMP

cost-effective methodology, DOE will apply concepts from two ASTM International standard practices,